just losses

-

I am very new to this area....... I have automated some strategies (London daybreak, SMA cross over pullback, intrabar momentum and..... ) with the help av Fxdreema and I can see on the tester that the EA is functioning according to the rules of these strategies and my money management is not so bad.... but nothing give me constant profit ........ Please could someone give some hints or introduce some good strategies that I can try to automate? Thank you very much for your help:-)

-

Hello Piroozmand,

i'm new too in strategy automation and i have to agree that is difficult to have results. The London daybreak is profitable for me, but my EA is still very rough and needs fine tuning and optimization.

What i did to have results is consequence of an error... my first version wasn't able to close the trades and i saw that some of them were going dramatically in profit if they were to the "right side". So i began to change the EA in something hybrid... and i'm not being able to do it yet because i can't undestand a lot of the "trailing stop" block functions.... If i use pips it's ok, when trying with % of various things it becomes difficult to understand how things are working.

Anyway the concept is that the London opening is presented as a 1/1 or 2/1 R/R intraday strategy, and results are not so good. But... what if don't use TP at all? Imagine to work with a 2:1 "virtual TP"; when price reaches TP your SL goes at TP/2 and your 1:1 is ensured. Then you start trailing with large parameters leaving the EA to follow the price as long as needed. Backtests seems to be promising in this way.Another thing i discovered while backtesting is that seems to be a "non sense" to trade a % of balance as risk. That's because, even if you are using a 4:1 R/R strategy, when you have a serie of losses, then you are no more trading the same amount of money and your 4:1 is no more true. It seems to be far better to trade fixed lots unless you find a strategy with a very high number of winning trades.

I'm curious to know other user's experiences too

")

-

Hello Malfy,

Thank you for the feedback:-)

I use the rules which is described by Joshua Martinez, easy to find on the internet. I use 1% of equity for getting the lot size and the R/R is always over 2. I close the trades at 20:00. I have tried both with and without trailing stop with different variables. But when testing the EA with historical data in 2016 it shows profit until Brexit and then it is just losses. I am really disappointed. But it is interesting about the idea of not using TP at all and let it go if it goes your direction. Do you get profits also after Brexit? -

I don't remember exactly what happened during brexit, but it was at night so probably the ea wasn't working because i'm closing loosable trades at 18.30 of each day.

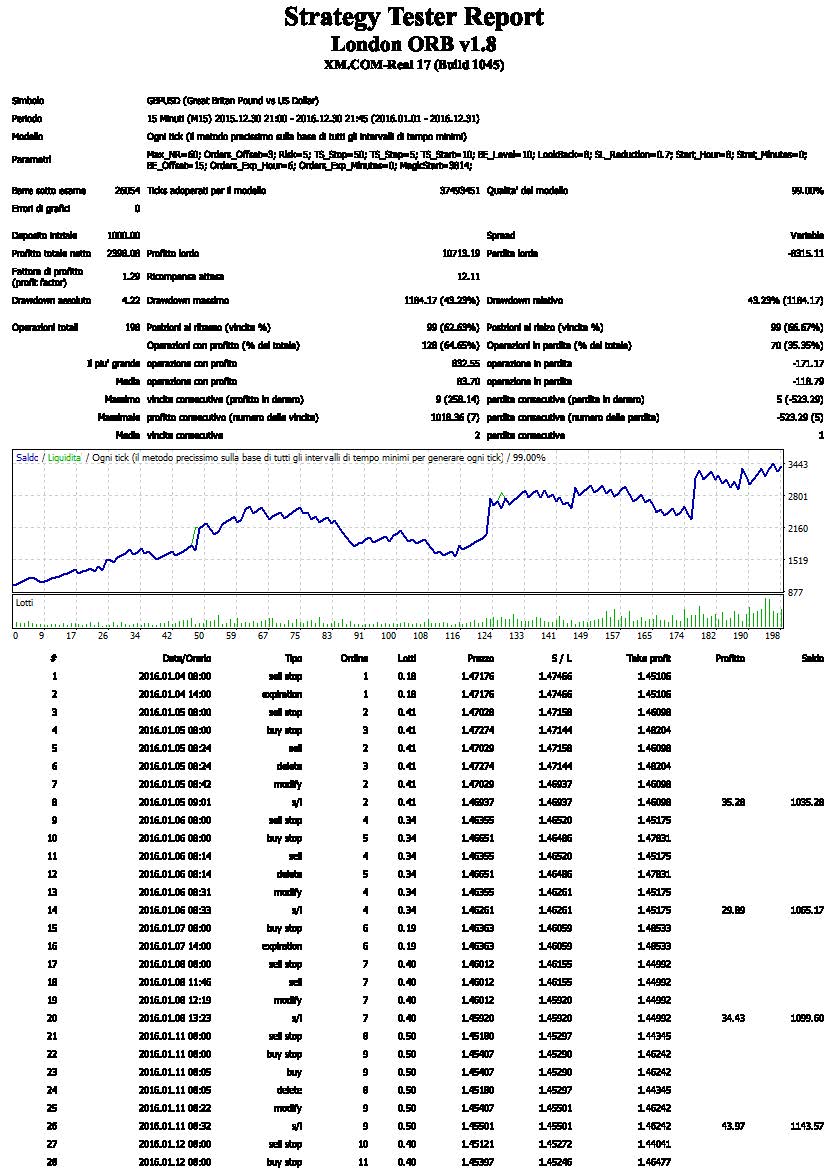

Anyway... this is my result for 2016... still far from any kind of optimization.

I'm using parametric lookback time, parametric orders offset (to avoid fake price moves) and also an SL reduction factor, because i saw during backtests that often when the price goes down over 50% on the negative side it doesn't come back.

EURGBP also gives good results but night ranges are smaller, it seems every pair needs a dedicated optimization.

Anyway... i'm still working on it.I'm also thinking about an EA based on the same principle but "always on"... i mean, something that is continuously looking back for a number of bars, checks the range and when the range is low enough places the pendings for a breakout.

It can be a good way to trade a 5 minutes chart, maybe using Ichimoku to predict a probable breakout direction. But at the moment it's too complicated for me... i need to practice a little more -

My knowledge is inadequate and I don`t know anything about parametric lookback time, parametric orders offset.... should study a little about it...

-

I guess what he means in "Parametric" is using a Parameter (constant) that's all

-

Yes eranger

You got it. I mean they are input parameters... nothing special. -

can you give me a little hint on how looking back can contribute to changes in the EA for better results?

-

When you look for this strategy on the net, you find that someone says to start measuring the night range from 23.00 of the previous day, someone else says you just need 4 hours before the session opens... someone else talks about just half an hour before.

So... the better thing to do, imho, is to assign a constant to the candle ID that you are looking back. In this way you can do multiple backtests or run the optimization to find what value works better.

Same for the start time... you can see if is better to shift it a little backward or a little forward.

Nothing changes about the EA behaviour, it's just a matter of tweaking it. -

... nice , I have now something to work with and try to optimize the EA..... a way to go before forward testing......

THANK YOU