Profitable test results on Falcon and Condor, and forward testing looking good

-

Below results are the latest backtests for the CONDOR V1 made with FX Dreema. My previous project was the FALCON V1 which is also looking similarly good, but CONDOR uses different logic.

I'm pleased to say thankyou so much to FX Dreema crew for creating such an outstanding program which allows making trading robots easy. While it hasn't been completely easy and a steep learning curve, it is very possible to navigate a program like this to make profitable trading robots. I have several already.

I'm pleased to say forward testing on demo is looking very good at this stage, however I've had to make some adjustments during the week after noticing a few glitches that didn't show on backtest, in order to have it work properly. I'm looking forward to seeing the results in the coming days and will post the forward testing results in discussions here.

I am protecting settings detail at the moment in given images.

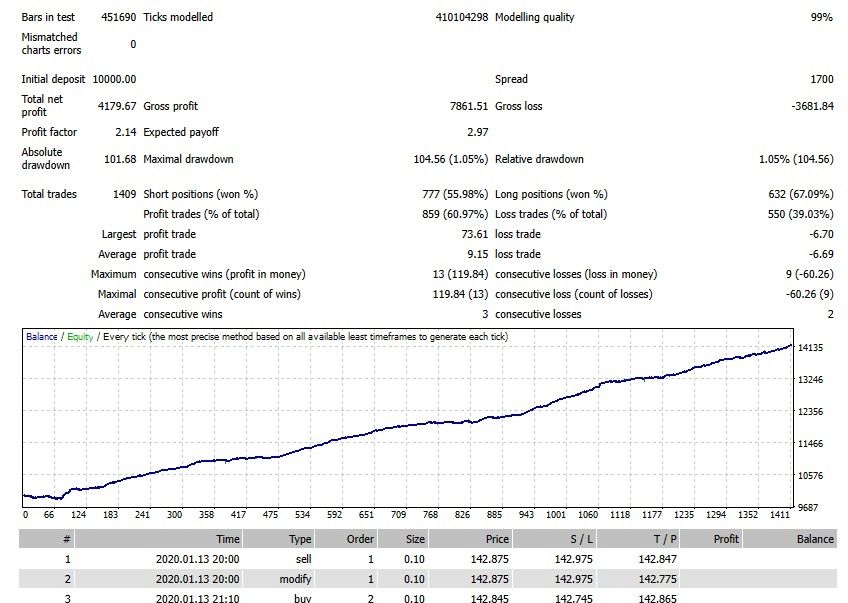

GBPJPY 4 year backtest - MT4, conditions: Every tick, M5 chart, total trades: 1,409. Accuracy of data 99%.

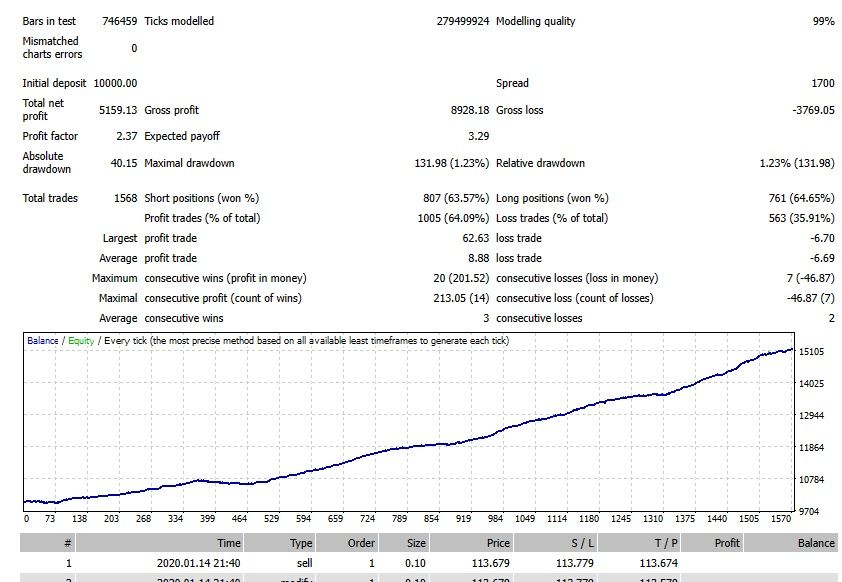

Below is CHFJPY 4 year backtest for same period, 1,568 trades total. This robot will give similar results for all the YEN pairs, and several USD pairs too. It will also work on M5, M15, M30 or H1 chart, however it generates far less signals on the higher time frames.

Now let me give clues as to the trading logic - Let's assume that the end of the NY session puts certain pairs into a trading range while the market prepares for the open of Tokyo market. There is a period of time when the market is ranging, therefore we take advantage of this period by trading ranges. Not trends.

Because ranges are more predictable, so we look at the highs and lows of this time of day and trade accordingly. We trade only SHORT positions when the institutions close their positions for the day in the initial hour. We trade only LONG positions prior to the open of the session. How do we know this? Well we can see it on the deep analysis tool that is SQ analyzer.

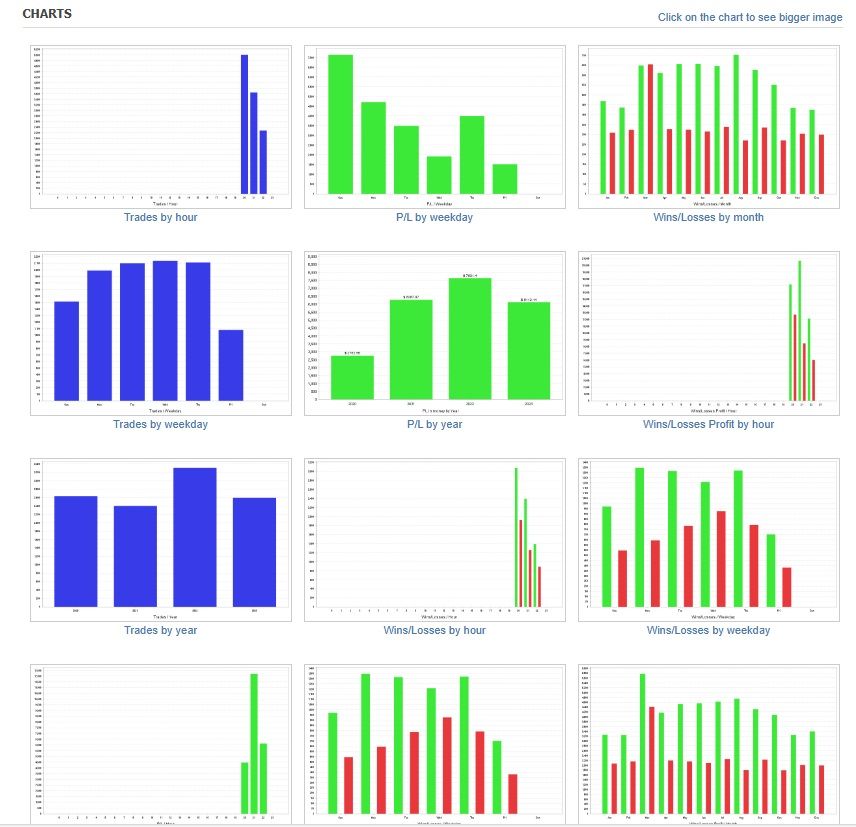

Hence a given report here details how a portfolio of JPY pairs would perform in the 4 year period. We can see that the very first month was a loss, but every subsequent month in the 4 year period was profitable. It is a simple matter to just sort the data and optimize the performance during the profitable periods of the day

I will post forward tests here in a week or two, stay tuned, and I am happy to answer any questions

-

You are looking to sell these or give these away at some stage

-

I won't need to do that. I'm sharing my experiences here and show how I get the results, once I have solid forward testing data that backs up my strategy

-

Even if there is no theoretical limit to the performance of an EA, that of such a simple strategy seemingly, looks a little to good to be true.

The good results might be caused by the "tester grail inaccuracy".

Are you using stop levels ? -

@seb-0 What is tester grail inaccuracy?

-

@seb-0 Yes, I’m definitely using stop levels. This is not a grid trading or hedging system. So there shouldn’t be drawdowns. I’ll make an edit to my post with Q and A

-

@Ipod I can't edit the post now.

Here's Q & A on the robot:

1. Does your strategy use stop losses or is it grid or hedging system?

No it's not a grid or hedging system. It definitely uses SL and TP's. The SL is fixed value while the TP is dynamic and has a minimum stop level equal to the SL

2. What indicator does it use?

It depends which robot you're asking about. The Falcon uses simple moving averages of candle highs and lows to compute the best levels to buy and sell the asset at any given time. The Condor uses bollinger bands to find the best trade entries to trade to the centre line

3. Why is the equity line so smooth, why do backtests look so good?

The creation of a reliable successful robot is really not that difficult. You probably have many robots that are profitable, but you aren't finding the profit because it hasn't undergone deep analysis. What is deep analysis? It is the careful meticulous inspection of how, when and why the profitable trades come and are you filtering them out properly? For example, the market trends and ranges. There are hours of the day where it is profitable, days of the week or months of the year. Is it profitable on longs more than shorts? Do you know this kind of detail? If you can study this then it can make all the difference. I've spent more time researching the exact times, ways and directions of trades that are profitable so I can isolate them. I use Strategy Quant EA analyzer but there are other programs out there to deep analyze the backtest reports

4. What time frame does it trade on?

The Falcon uses M5 time frame only. The Condor can be traded on M5, M15, M30 or H1 time frames. It is equally as reliable on any time frame

5. What assets can be traded on?

Generally both robots can be traded on JPY pairs and work the best on JPY. The best performance comes from CHFJPY, GBPJPY and NZDJPY, followed by EURJPY, CADJPY, AUDJPY and USDJPY. The Condor can also handle some USD pairs like GBPUSD, EURUSD.

6. What is the profit factor?

Profit factor is total gross losses (losing trades) divided into total profitable trades. For example if the total losses are $100 and the total profit is $150 then the PF is 1.5. Anything above 1.0 is profitable. The profit factor for this robot is anywhere from 2.00 to 2.7 depending on the pair. In the earlier data I could achieve a PF of around 4.5 but it had many fewer trades so I'm trying to balance having a good profit factor with a good volume of trades. Maybe that's something I can put in the settings as a preference.

7. All your backtests are the last 4 years. How stable is the robot long term?

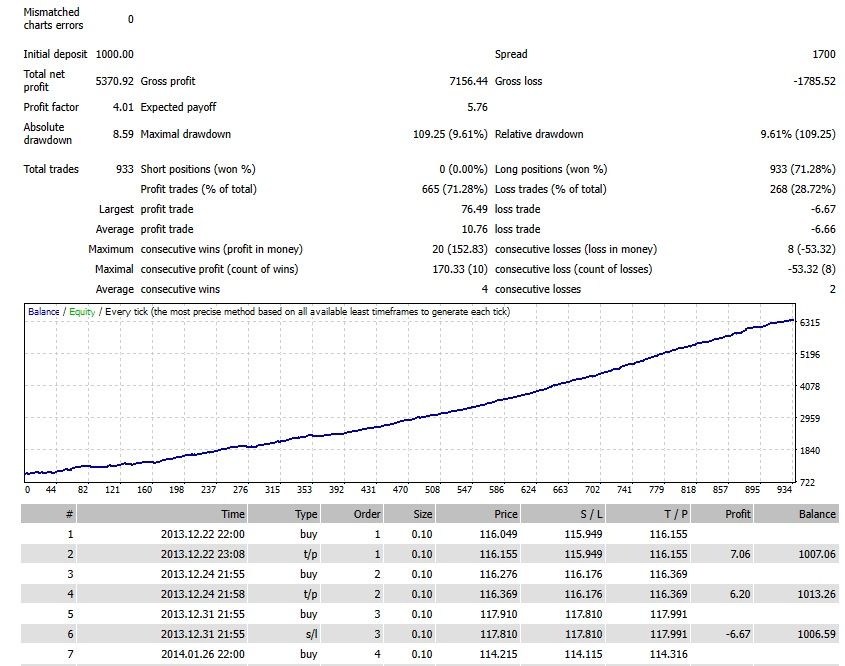

So I decided to do a 10 year backtest for the Condor just to see how it does even though my main tests have been 4 years. Here's my 10 year backtest for CHFJPY:

That's about all the Q's I can think of. If anyone has any more I'm happy to answer them

-

Let me guess: the dynamic TP is the one factor that is utmost important for the EA. The moment you test using fixed stops, the EA plummets?

Need small help? Tag me in your post

Need big help? https://www.fiverr.com/big_algo/automate-your-winning-strategy-in-mql4-or-mql5 -

Try replacing buy trades with sell trades and vice-versa, so it will be the exact opposite strategy. If it is still profitable that's a bug.

-

@roar No, if you use fixed SL and TP the robot is still profitable. The win rate is between 60-65% and that's with some TP's on trades being higher than SL. Hey, I tried to do backtest using MT5 but I can't seem to get the tester working. Can anyone backtest on MT5 for me?

-

@roar I finally got MT5 backtest working. Here is CHFJPY, for some reason it's not taking as many trades

-

Try that on forward testing for one year and bring the results back. If the chart is even close to that, I will put my money on it. Meanwhile, thank you for the info, but it's too good to be true.

-

@Ipod

I haven't investigated how it works exactly but : In live the stop levels will be placed on the broker sever side, and the price will be modeled based on them(based on the stop level that will be triggered). When you use stop levels on the tester, the price is modeled discontinuously(as live), independent of these stop levels. Then on the tester the price jumps from one point to another that are never(almost) exactly at the level of these stops. And here I lack knowledge, I don't know if it's enough that one stop level gets triggered, and if it's a TP it will be at the level above(level of price modeling), if it's a SL at its exact level. Or if it must trigger both stop levels and then it will always consider the TP was triggered first.

I think roar knows. -

@seb-0 the "TP or SL trigger choice problem" might not be the reason here, as there is supposedly always min 20 pips difference between those levels.

I am very interested in this, but purely from the point of figuring out where the tester goes wrong, in what detail does the devil hide...

@Julianrob your mt5 backtest shows much larger "largest loss trade" while the mt4 backtest seems to have a fixed SL, largest being the same as average. -55 vs -6. So there is some different trading logic going on.

-

I have created bots that mimic backtest results on live trading, win or lose, when backtesting over the same time period that live trading was ran for. Not common but one of my tests for a possibly good bot.

-

@seb-0 I don't think there's much discrepancy with stop levels on backtest versus forward test, unless its a small time frame like M1. If there are any issues that are hard to replicate on forward test or live, I'd say it's likely to be variable spread, or wide spread. But there's a spread filter on it which is kept slim. I don't like to be ripped off by the broker, I prefer to wait til the spread is narrow. So backtesting times when the spread is thin is very hard to replicate so I guess we'll see

@roar I can't explain that largest loss trade being so high because at micro-lots it should never be more than the average loss trade which in this test is 10 pips. There are a few strange quirks with MT5 backtest. All I can put it down to is perhaps that was a trade that gapped into loss more than the SL and I assume the tester takes the open bar price, not the SL price to close that trade

-

Well it's taken me longer to get some real time data forward testing as I've had to make a lot of unexpected changes to the trading robot in order to get it to work the same way on forward demo trading than how it's backtested. And now it will take me a bit longer than expected to get solid forward testing results as I've had to apply new filters to the trades since backtesting.

But, first impressions are looking good forward testing now. Today, here's a screen grab of 13 open positions, all in profit. I know it's not much real info yet, but first optics are looking good and confirming my strategy. This is the FALCON robot you see. I'm really getting a good feel for what certain assets do at different times of day

I will keep updates coming in future discussions

-

Is it confirming your strategy, though, if the same system doesn't work live but instead you need to add more filters...?

Can you show the results when you used live exactly the same system that you backtested?

-

@roar

Haha, assessing the profitability of a strategy with a single trading day, and managing to "feel" the market that quick is pretty nut also. -

@seb-0 The main reason backtesting is giving me inconsistent results is because it can't simulate the real spread variation particularly at the turn of the day. That is what I'm working on solving