Strategy Results, Good? Bad? Okay?

-

@roar

Haha you made my day

The stats look good to me also, but 2 years is still a pretty short period. I already experienced some EA with such results on short term, but it was something else on a longer period.

I don't know if these changes are due to "externalities" or if the market readjust itself, but it will probably not last for long.

But about your EA I don't really know I don't know how it works -

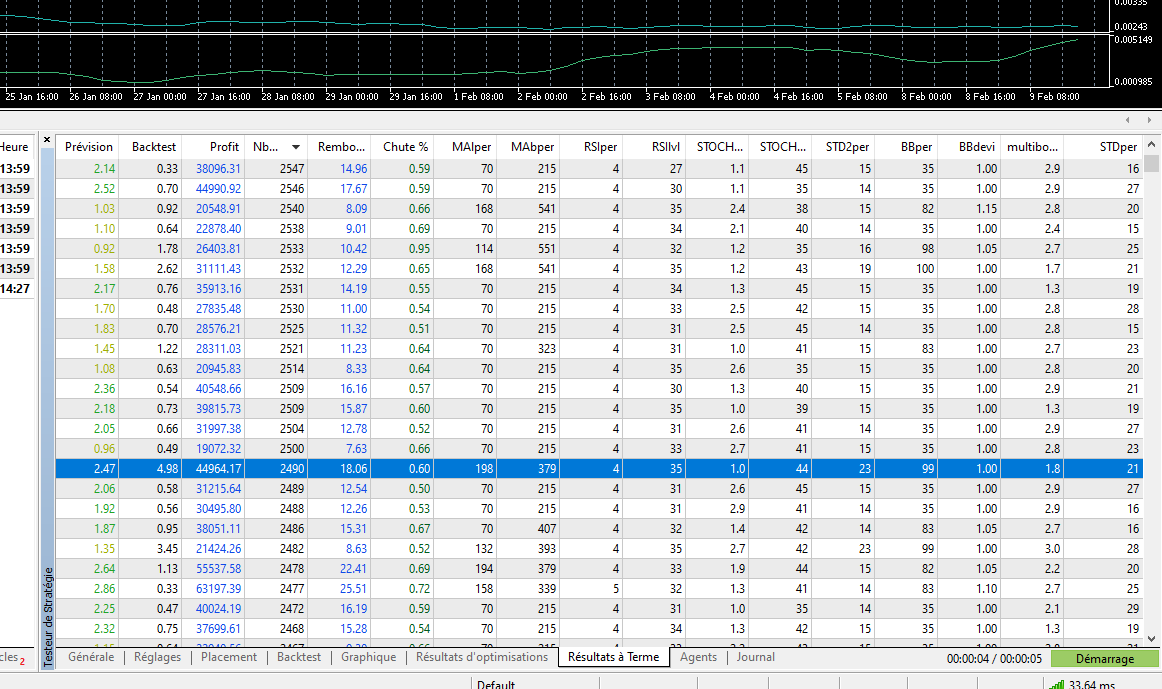

I'm doing some optimizing now, running on 20 cores on 3 shared computers. Trying to get my max balance higher based on changes in my entry positions, then I will reoptimize based on stoploss and take profit. If there is still 1 more optimization needed I think it will only need to work on drawdown percentage. I will throw on more years in between each process to see how it does but for now the last 2 years will be my focus. Thanks for the tips. I'll keep updates here

-

seeing how efficient an AMD desktop is at eating through these scenarios I'm almost inclined to do a total AMD build to take advantage of how they can use the GPU to accelerate the CPU process and visa versa. Whether or not the MT5 software will take advantage of it is unknown, either way though, the performance of their new chips would we worth the time it sits waiting for stuff to optimize.

-

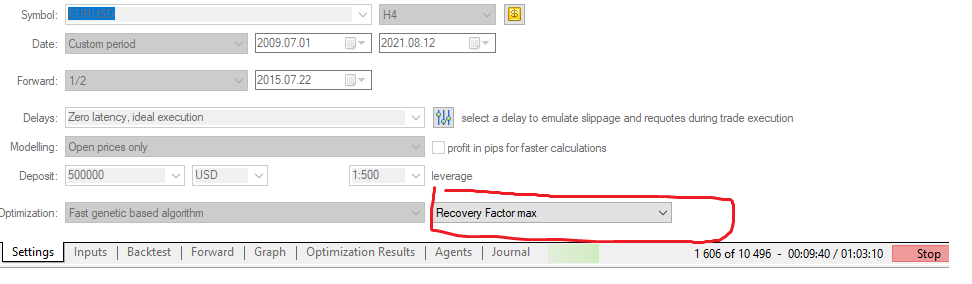

@jsauter86 for me, recovery factor optimizing works better than just balance, but that might depend on the strategy

Need small help? Tag me in your post

Need big help? https://www.fiverr.com/big_algo/automate-your-winning-strategy-in-mql4-or-mql5 -

optimized entries, added in 2017. Very obvious that take profit optimization is required and stop loss maintenance.

-

@roar what exactly is recovery factor optimizing?

-

@jsauter86 I mean the optimization algorithm in the tester, you use that?

Recovery factor = net profit / biggest drawdown

Need small help? Tag me in your post

Need big help? https://www.fiverr.com/big_algo/automate-your-winning-strategy-in-mql4-or-mql5 -

@roar I think its easier for me to think about in regards to what I'm trying to achieve. First optimize was to increase balance as much as possible. That to me was entries first, so I only checked to be able to modify 6 conditions in total and it took 1.5 hours to optimize. Next step is to increase profit and decrease drawndown by means of allowing it to optimize my hard stop loss and the trailing stop I'm attempting to convert to instead of the normal 2x ATR. With the second run I think it will be 4 paramaters and hopefully will only take 45 minutes to do.

Finally if a 3rd run is needed, I have the data from the last 2 runs that gave the top results in several categories. I will use all of the paramaters to make 1 final optimization. that encompassases all previous conditions in 1 run.

-

@jsauter86 fair enough, sounds good!

Need small help? Tag me in your post

Need big help? https://www.fiverr.com/big_algo/automate-your-winning-strategy-in-mql4-or-mql5 -

@roar i see you have forward selected, using a date from 2015...whats 1/2 forward for after that date going to chage?

-

@jsauter86 WOW! " Good" Please advise, what condition do you use? 555

-

@jsauter86 the genetic algo finds the best inputs using backtest information between 2009-2015. After that, it tests if those inputs hold in the "future", 2015-2020. If forward test fails, we know the good backtest was just luck ("overfitting").

https://en.wikipedia.org/wiki/Training,_validation,_and_test_sets

-

a single SMA zero value cross to determine direction, then price action for entries.

combined with time vs price as well as eliminating a few bad days. -

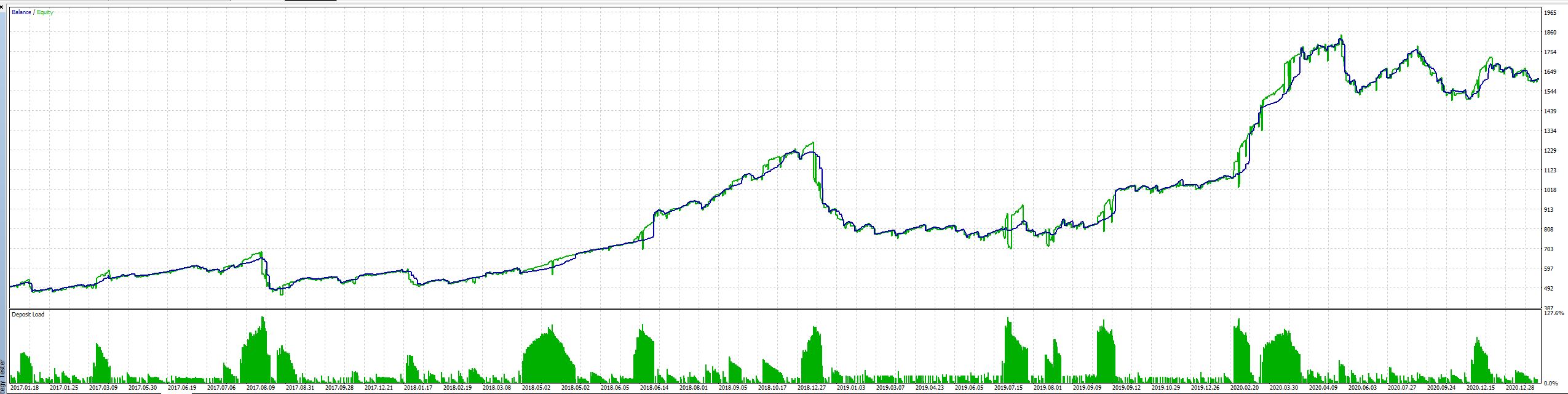

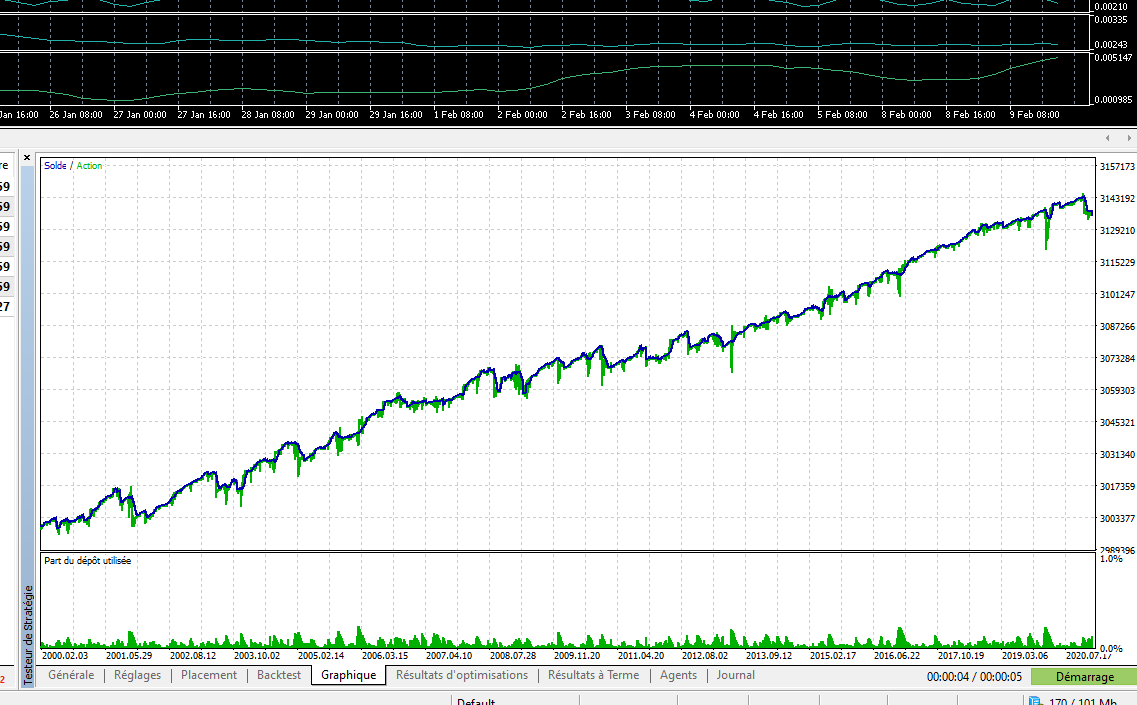

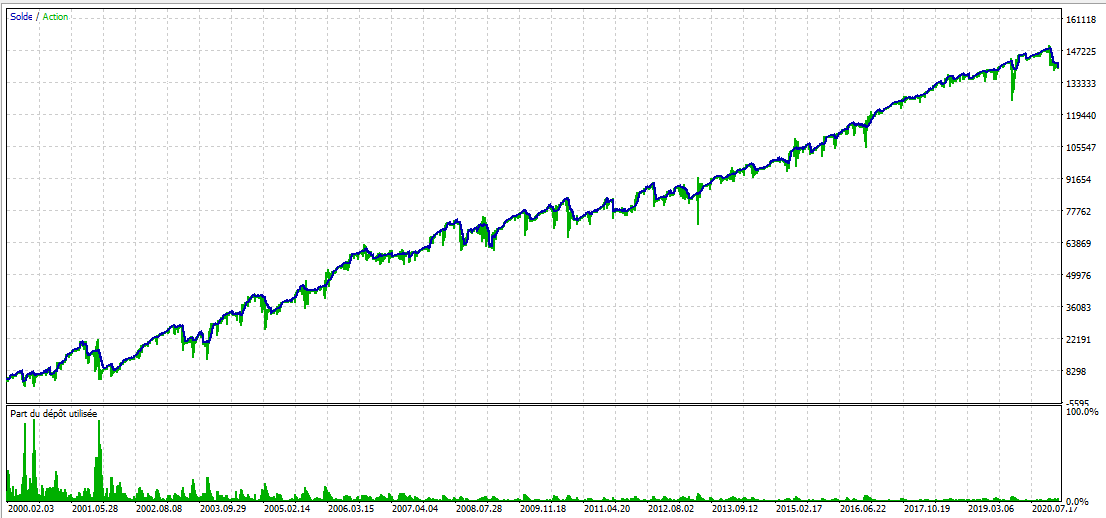

Here are the results of my current EA.

I tested it on EURUSD, from 2000 to 2021, on timeframe H4, forward on 1/3.

I think these are some pretty correct results because : I tested it on a long period; the number of trades is pretty important; and the majority of the backtest/forwardtest results were positive.

Just wanted to show you that")

-

@seb-0 Impressive results!

Can you show any myfxbook with those same results in real, please?

Can you show any myfxbook with those same results in real, please? -

@seb-0 that looks pretty good. How does it look with a reasonable amount of money to start with? Like...$500 USD.

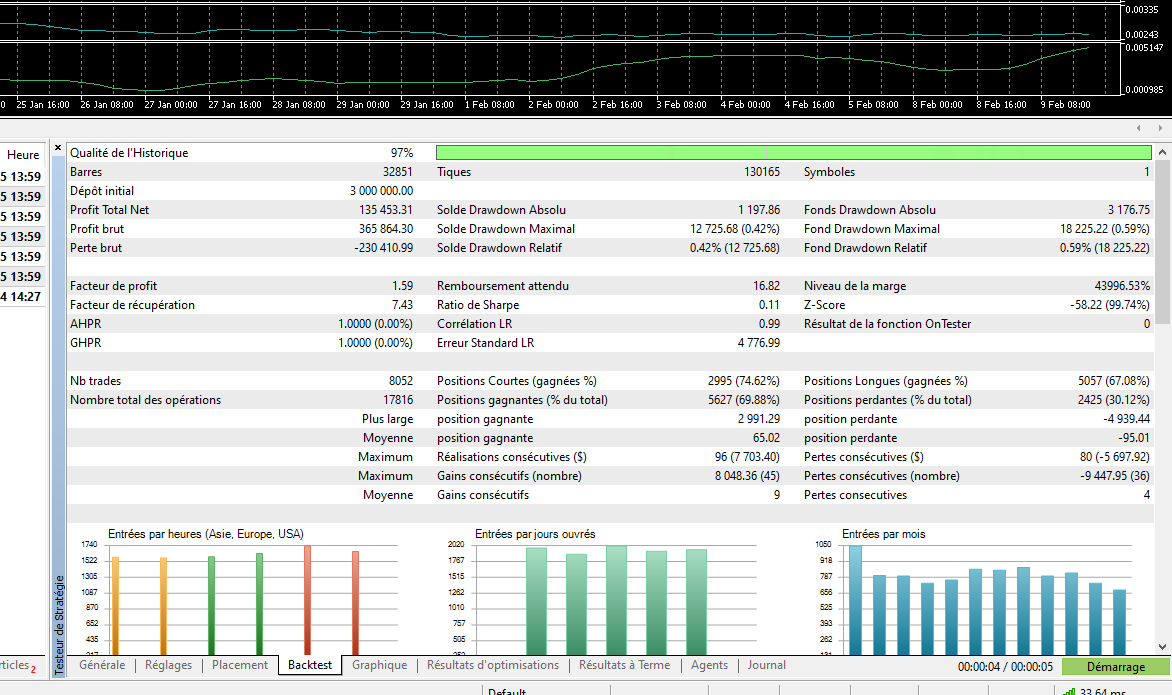

I'm also wondering how it only took 4 seconds to run that scenario.

-

@seb-0 Nice result. Put 50% of your money into this and 50% into sp500, and you probably get better Sharpe ratio than sp500 alone.

-

@l-andorrà Thanks! I never use this website, Ill have a look at it and update you if I do

@jsauter86 It takes only 4 seconds to test because it is pretty simple strategy using buffers, with no heavy calculation. Also you should select "simple" instead of "display" in the general tab of the tester, for faster test.

Here is the balance graph going from 5000€. I must start with as much not to blow my account, with a fix amount of lot at least :

-

@roar

I was planing to run the EA on 2-3 instruments for diversification, but on Forex only.

So you recommend me also to go long on the sp500, not through the bot ? -

@seb-0 sp500 is closely related to EURUSD, usually a strategy that works on EURUSD also works on sp500. The goodness of the strategy is there but for a more credible test it simulates withdrawals at least once a year and, not negligible, the drawdown that is psychologically sustainable for you.