What's the accepted profit factor when backtesting an EA?

-

as above, for those expert senior that creates good EA, for a guideline for us newbie to set the standard - what is the good profit factor point to denote a possible profitable EA?

-

I would say As higher as better.

If your strategy is profitable for a certain period of time, you will have a PF > 1. So, as an average, for 1$ invested, you will get more than 1$ what let you have a consistent profit.

I reject trading strategies with a PF < 1.3 in a determined period of backtest (IS). That value means that you have a 30% of profit for each 1$ invested as an average. But this is my way to rate the strategies.

-

I don't look the profit factor at all. If you optimize by profit factor, many times you end up with only 10 trades, no losing trades at all. It is not a reliable result, because 10 trades can be coincidence.

My first criteria is number of trades. If you can make 200 trades (in about 1-3 years) and still be in profit, that is much more reliable result.

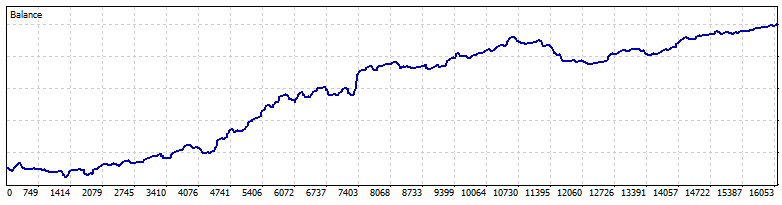

Second factor is drawdown % relative to max profit (the recovery factor). Don't make those EAs that go a straight line up and then boom 100% loss.

I prefer a graph like this - steady up, no big spikes down, lots of trades:

Also, if you optimize your parameters, use half-period to find the parameters and other half-period to test the optimal parameters. Thats the scientific way

-

Todo lo anterior esta muy bien teóricamente, pero la realidad es que luego entras en real y no tiene nada que ver, y lo normal es que pierdas dinero, por lo menos, eso es lo que me pasa a mi, mucho backtesting, profit factor............., pero al final no soy capaz de ganar dinero en real.

-

@LUISRI You are right and real environment might be different to Demo or Backtest. But you will agree with the fact that if a strategy has a good behavior in backtest (IS & OOS) and in demo it does not behave exactly as in backtest but close enough, that strategy might have some edge on real.

@roar I totally agree with you. There are other values to look at to be sure that a strategy might be consistently profitable and its behavior is statistically significant.

-

Yo al principio con lupa, pero la realidad es que cuando pones el ea en real, es que no tiene nada ver, ademas os voy a decir una cosa, si fuera tan fácil uno cosntruia o compraba un ea y ganaba mucho dinero, y por desgracia no debe ser así, sino habría mucha gente millonaria, y la verdad que es mucho mas difícil de lo que parece. Yo llevo 12 años en esto y de momento aspiro a ello, pero de momento no lo he conseguido.

-

thanks for the inputs! i observe a period of 8 years and pick the worst performing year to fine tune the strategy (not using the mt4 optimizing option). I also learn to accept trades that is lose in the beginning and tried to use other controlling methods or TS to reduce the losing pips (=pips saved).

once the EA passes 8 years (historical data), i will use 3 years prior to that 8 years or after that to test on data which is never used to observed. (is this walk forward test?) Since the EA isnt scalper based hence i think 99.9% isnt needed?

I would like to learn some advance theory of methods to enter/filter trades and hope seniors here and share some directions? any tips on making a scalper EA that makes +/- 5%?

many thanks Sirs!